USAA serves a concentrated military-affiliated population across the St. Louis metro, with the densest cluster around Scott AFB on the Illinois side. Storm and heavy-rain claims under USAA follow the standard HO-3 framework: water that enters through a wind-created opening in the building envelope is generally covered; surface water and foundation seepage are excluded. USAA-specific scrutiny on cause-of-loss timing applies on storm files just as it does on burst pipe files, which means the wind-driven-rain narrative needs to be airtight. Flood from rising water requires separate NFIP or private flood coverage, and a large share of the homes around Scott AFB sit in or near mapped flood zones where this gap matters.

How USAA handles storm and heavy rain claims

USAA uses a mix of in-house staff and independent adjusters on storm files, with photo-based desk adjusting common on smaller losses. Estimate review runs 5-7 business days from receipt per USAA guidance, with payment following in 3-10 business days on non-CAT losses. Roof inspections are typical on wind-driven rain files because the cause-of-loss determination depends on documenting envelope breach. The PDRP network (Accuserve, Rytech, Crawford Contractor Connection) handles direct bill for enrolled contractors. Per USAA materials, policyholders retain the right to use any licensed contractor. Gateway is not enrolled in the PDRP and writes Xactimate-compatible estimates that bill through to the member. NFIP claims, where the loss is flood rather than wind-driven rain, run on a separate timeline and policy.

Common denial reasons for this kind of claim

The leading denial on USAA storm water losses is the standard wind-driven-rain versus surface-water reclassification, made stricter by USAA’s documented scrutiny on cause-of-loss timing. Without photo evidence of envelope breach the surface-water exclusion applies. Flood losses (rising water) are denied under the HO and require separate NFIP or private flood coverage to be paid. Maintenance-related roof failures (aged shingles, deteriorated flashing) get pushed into the maintenance bucket. Mold-related portions are denied where mold is deemed pre-existing or maintenance-related rather than stemming from the storm event. Gateway pulls NOAA storm event data for the loss date and ZIP, photos the envelope breach from a safe vantage, and documents water path from entry through assembly.

What Gateway documents differently

For USAA storm files Gateway pulls NOAA storm event data for the property address and loss date, documents envelope breach with date-stamped photos, and traces water travel from entry point through the building assembly. The Xactimate scope separates wind-driven rain remediation from any flood component the member may need to address through NFIP. Photo organization is tight to support USAA’s photo-based desk adjusting pattern on smaller files. Where the home sits in or near a mapped flood zone, we flag the NFIP/HO coverage line up front so the member is not surprised when surface-water portions are excluded under the HO.

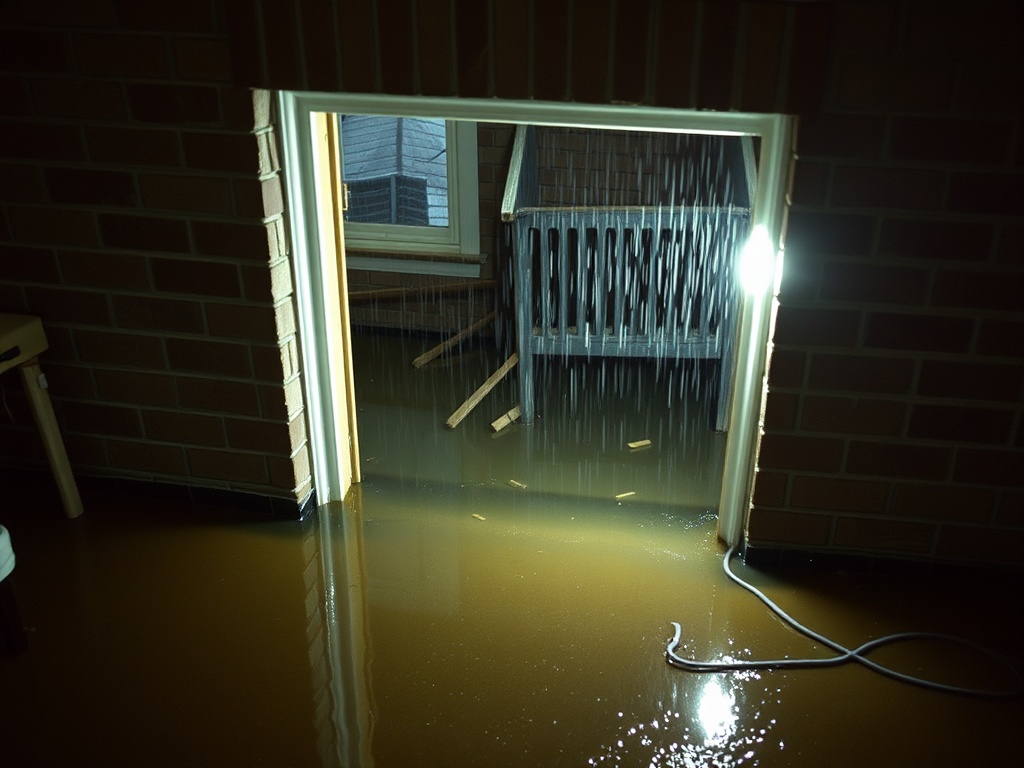

Will USAA cover flood damage from a storm?

Not under the standard USAA HO policy. Flood from rising water requires separate NFIP or private flood coverage. Water that enters through a wind-created opening in the roof, window, or wall is generally covered under the HO. The distinction is critical near Scott AFB and other St. Louis metro areas with mapped flood exposure. Verify your flood coverage status separately.

How does USAA handle wind/hail deductibles in MO and IL?

USAA files separate percentage wind/hail deductibles in many states where they are applicable per state filing. In hail-belt MO and IL ZIPs, a percentage deductible on Coverage A may apply on storm losses even if the all-perils deductible is flat. Your declarations page will state the deductible structure. Verify your specific policy before estimating recovery.

Will USAA pay for mold from a storm leak?

Per the USAA homeowners policy summary, mold is excluded as a primary peril but mold removal incidental to repairing a covered water loss is addressed in the course of that repair. State-specific sublimits and endorsement options vary. Mold deemed pre-existing or maintenance-related rather than stemming from the storm event is excluded. Verify your specific policy.

Free Tool

Build your claim documentation checklist.

Pick your insurance carrier and claim type. We’ll generate a carrier-specific list of what to document, what to photograph, and what your adjuster will look for. Based on Gateway’s observed workflow with each carrier (not legal advice).

Want Gateway to handle the documentation for you?

We photograph, measure, scope, and submit. Direct-bill where the carrier allows. You pay your deductible, we invoice the rest.

Call (314) 947-3419More USAA resources

Other USAA pages

on Gateway.

USAA storm and heavy rain claim. Call now.

Live phone, twenty-four seven. We’ll dispatch the nearest crew and start the documentation the moment we hang up.